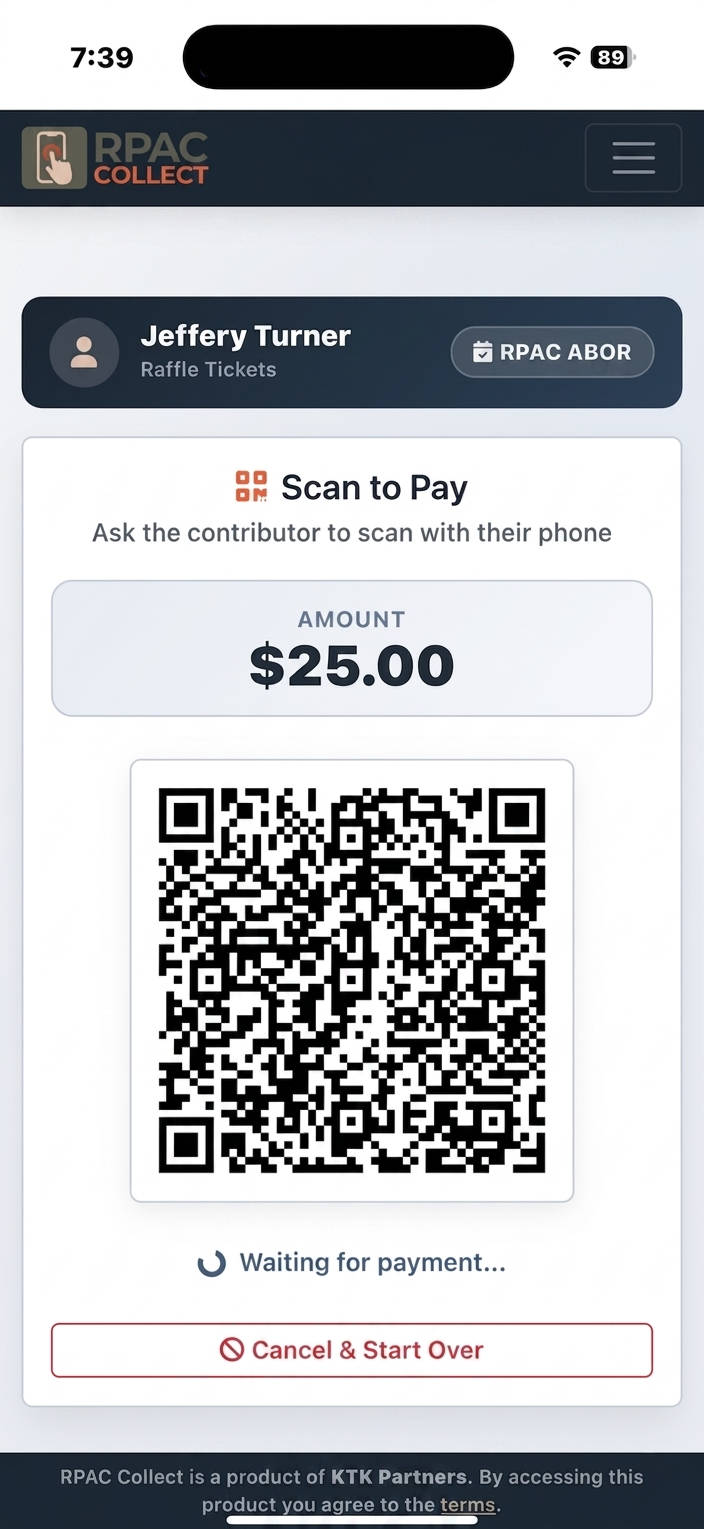

For REALTOR associations

Real-time RPAC collection

from the phone in

your pocket.

No Square readers. No paper forms. No uploads. A standalone app any approved collector can use to take a contribution from any REALTOR at any event, routed through NAR e-commerce to your state RPAC account in seconds.